Why Your Credit Report is Important

Right To Dispute Errors

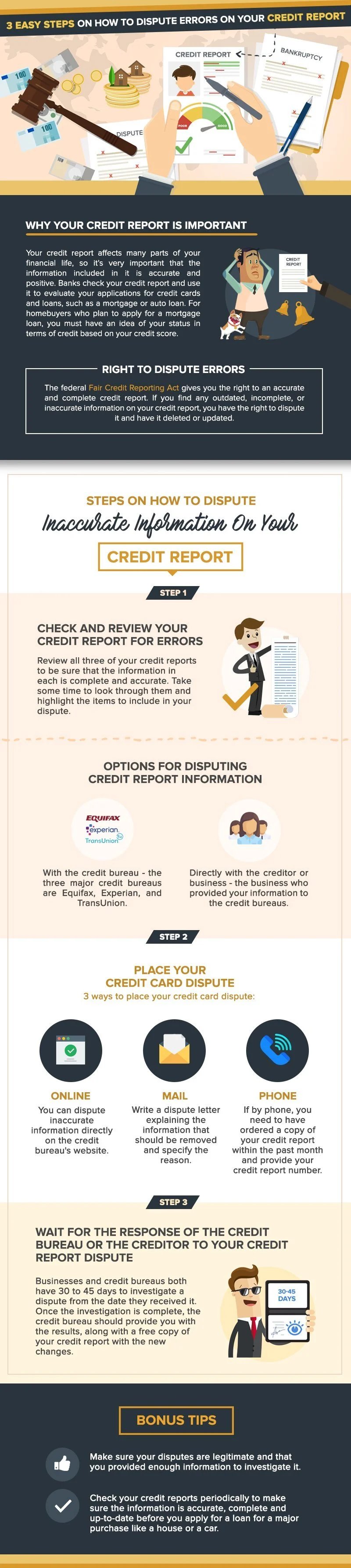

However, it's very common for credit reports to contain errors, and these occur for a number of reasons. Some of the information that could mistakenly end up on your credit report can be anything from inaccurate late payments, to even a falsely reported bankruptcy.1. Check and Review Your Credit Report for Errors

The best way to find any inaccurate information on your credit report is to check a copy of it. There are several ways that you can get a copy. You can even get a free annual credit report from each bureau through the AnnualCreditReport.com, or order one directly from the bureau.Credit Report Errors You Can Dispute

You can dispute credit report items that are inaccurate, incomplete, out of date or that which cannot be verified. It can vary from minor and innocuous errors such as a misspelled name, an old address, birth date or your social security number. However, other errors could be detrimental to your credit score and could potentially cost you tens of thousands of dollars.-

With the credit bureau, the company responsible for compiling your credit report based on information received from your creditors. The three major credit bureaus are Equifax, Experian, and TransUnion.

-

Directly with the creditor or business who provided the information to the credit bureaus (also known as the information provider). You may do this when the credit bureau responds that the error you disputed was verified by the creditor.

2. Place Your Credit Card Dispute

Here are 3 ways to place your credit card dispute:-

Online - Disputing credit report errors online is probably the most convenient way. You can dispute inaccurate information directly on the credit bureau's website. Each credit bureau should provide a way to upload, fax, or email documentation supporting your dispute. You can also check the status of your dispute online by providing your confirmation number. However, you can only get the results online and not by mail.

-

Mail - Placing your dispute by mail takes more time, but it provides you with the paper trail you’d need if the credit bureau doesn’t respond in a timely manner. You must write a dispute letter explaining the information that should be removed and specify the reason for why it is inaccurate. Also, include a copy of proof of the error and other supporting documentation (not the original copies). Send the letter via certified mail with return receipt requested so you’ll have proof of when you made the dispute and when the creditor receives it.

-

Phone - To dispute by phone, you need to have ordered a copy of your credit report within the past month and also provide your credit report number. However, you’ll still have to mail in any documentation or proof that supports your dispute.

3. Wait for the Response of the Credit Bureau or the Creditor to Your Credit Report Dispute

Businesses and credit bureaus have the same amount of time to investigate a dispute — 30 to 45 days from the date they received it. Once the investigation is complete, the credit bureau should provide you with the results, along with a free copy of your credit report if there had been some changes. If they don’t respond in that time frame, you have the right to sue in Federal court for up to $1,000.-

Make sure your disputes are legitimate and that you provided enough information to investigate it. Be careful not to do anything to make the credit bureaus think your credit report disputes are frivolous. Don’t dispute everything on your credit report and don’t send all your disputes at once. Also, avoid disputing an item multiple times. The credit bureau or the creditor can determine that your dispute is frivolous or irrelevant if you don’t give them enough information to investigate the dispute. They also have every right to reject it.

-

Check your credit reports periodically. Financial advisors and consumer advocates suggest that you review your credit report periodically to make sure the information is accurate, complete, and up-to-date before you apply for a loan for a major purchase like a house or car, buy insurance, or apply for a job. Likewise, when applying for a mortgage loan, improving your credit score will give you a better chance to get pre-approved, which is the first step in purchasing your dream home.